Income is liquid fuel to a financial plan. A Cash Flow Table helps guide the Personal Financial Statement in the right direction.

The end of the month is pay day for many. This is an exciting time because you’ve earned the opportunity to either invest towards the financial plan, or realize benefits today. In reality, it’s probably a mix of both (let’s be honest, a little bit of fun too is healthy, right?) and it’s vital to plan proactively to know the right balance and avoid asking, “wait, where did my money go?”.

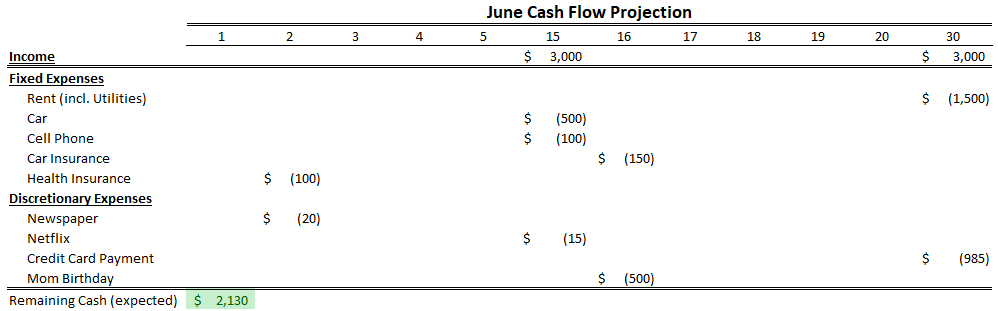

Maintaining a simple Cash Flow Table like the one below helps forecast cash needs into spending buckets with due dates. Visuals like this create a road map for how much cash is needed for what and when so it’s not accidentally spent on something else. There are many online services out there already to help maintain this data on your behalf so be sure to explore a bit.

Organizing cash flow into spending buckets is important because it highlights how flexible incoming cash is. Implicitly, you’ve already committed portions of your income to be spent on fixed expenses (long term obligations like rent, car payments, utilities) and discretionary expenses (short term obligations that can be easily changed like entertainment, travel, hanging out) – ultimately this shows how much income you actually have power over.

Ideally there is cash remaining each month that can be allocated to fun things (a vacation, eating out at a restaurant, etc) or the future (saving up for a car, HSA contributions, or retirement plan contributions). If not, the expenses need to be adjusted and perhaps maybe it’s time for a change in lifestyle. If so, the extra cash is your dry powder that you need to plan for. This should inspire some reflection on your behalf. Some things to ponder:

- Is my current lifestyle within my means or too expensive?

- Is what I’m paying for indicative of what I value?

- Which expenses do I need to plan for paying that may exceed my income in a month?

- How much fun can I afford?

The answers to these questions will vary from person to person. Have the conversation with yourself on what matters and how much it matters. That conversation will inspire you to create/adjust/confirm a budget that’s aligned with your values. Your income is the easiest way to direct a successful financial plan so be in charge of it!

Compliance stuffs

Just remember, I’m not your financial advisor so the information may or may not best apply to your situation and you should get formal advice prior to doing anything. The information/data that is shared should be double checked by you and any conclusion that is driven based on past data is not to be interpreted as my advice for your future. I will do my best to only write what I think is true and right, but mistakes happen and we’re all learning together – this is meant to be an informal conversation.